Page 133 - Maths Skills - 8

P. 133

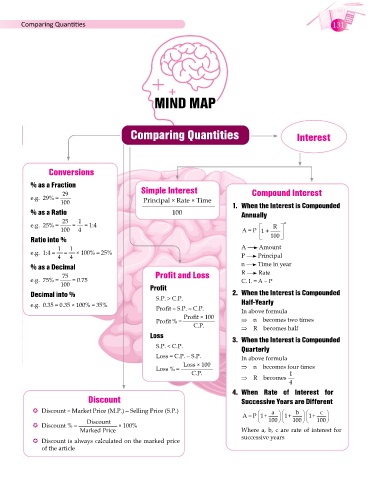

Comparing Quantities 131

MIND MAP

Comparing Quantities Interest

Conversions

% as a Fraction

29 Simple Interest Compound Interest

e.g. 29% =

100 Principal × Rate × Time 1. When the Interest is Compounded

% as a Ratio 100 Annually

25 1

e.g. 25% = = = 1:4 R n

100 4 A = P 1 +

Ratio into % 100

1 1 A Amount

e.g. 1:4 = = × 100% = 25%

4 4 P Principal

% as a Decimal n Time in year

75 Profit and Loss R Rate

e.g. 75% = = 0.75 C. I. = A – P

100 Profit

Decimal into % S.P. > C.P. 2. When the Interest is Compounded

e.g. 0.35 = 0.35 × 100% = 35% Half-Yearly

Profit = S.P. – C.P. In above formula

Profit × 100

Profit % = ⇒ n becomes two times

C.P. ⇒ R becomes half

Loss 3. When the Interest is Compounded

S.P. < C.P. Quarterly

Loss = C.P. – S.P. In above formula

Loss × 100 ⇒ n becomes four times

Loss % =

C.P. 1

⇒ R becomes

4

4. When Rate of Interest for

Discount Successive Years are Different

� Discount = Market Price (M.P.) – Selling Price (S.P.) A= P1+ a 1+ b 1+ c

Discount 100 100 100

� Discount % = × 100%

Marked Price Where a, b, c are rate of interest for

successive years

� Discount is always calculated on the marked price

of the article